SUMMARY

Property development finance is a specialised structured loan that funds ground-up construction projects from land acquisition through to completion. It typically covers up to 70% of gross development value (GDV) or 90% of total project costs, with funds released in tranches tied to construction milestones. Loans run 12 to 24 months, cost 7% to 12% per annum plus arrangement and exit fees of 1% to 2%, and are repaid via sale of completed units or refinance onto a long-term mortgage. Security is typically a first charge over the site, a debenture over the borrowing SPV, and a personal guarantee from the shareholding directors.

Property development finance is a structured funding solution specifically designed for building new properties from the ground up. It provides capital to acquire land and complete construction of residential or commercial buildings, with repayment typically occurring through sale of the completed units or refinancing onto a long-term mortgage.

This finance type differs fundamentally from standard mortgages, which require a completed, habitable property. Development finance instead provides structured funding throughout the construction phase, supporting projects from initial land purchase through planning, construction and final completion.

Key characteristics:

Term length: Typically 12 to 24 months depending on project complexity

Funding structure: Staged drawdowns tied to construction milestones

Security: First charge over the development site, fixed and floating charge over the borrowing SPV, and personal guarantee from the shareholding directors

Exit routes: Sale of completed units or refinance to an investment or commercial mortgage

Borrower profile: Experienced developers, builders and property investors

Most commonly used for:

Ground-up residential developments (houses, apartments, multi-unit schemes)

New-build commercial properties (offices, retail units, industrial buildings)

Land subdivision and infrastructure projects

Conversion projects requiring substantial structural work

The three key numbers that define your loan:

1. Gross development value (GDV): The estimated market value of your completed project. For a four-unit residential scheme where each house sells for £350,000, your GDV is £1,400,000.

2. Total development costs (TDC): The complete cost to deliver the project, including land acquisition, build costs, professional fees, statutory fees, finance costs and contingency (typically 10% of build costs).

3. Loan-to-value (LTV) and loan-to-cost (LTC) ratios:

Up to 70% loan-to-GDV: maximum borrowing based on end value

Up to 90% loan-to-cost: maximum coverage of actual project expenditure

Deposit requirement: usually 30% to 35% of land purchase, or 15% to 20% of total project costs

The lender calculates both metrics and lends the lower amount, ensuring the project remains viable with an adequate equity buffer. Each lender has a different metric.

Staged funding: how money flows through your build

Unlike a traditional loan where you receive funds upfront, development finance operates through controlled drawdowns aligned to construction progress.

Typical drawdown stages

Initial advance (land purchase): 65% to 70% of land cost released on completion of legal purchase

Foundations stage: Released once concrete foundations are complete and inspected

Ground floor / first fix: Funds released when structure reaches specific completion milestones

Roof stage: Released once the building is weatherproof

Second fix stage: Funding for internal finishing, services and fixtures

Practical completion: Final release on satisfactory completion inspection

Example drawdown schedule for an £850,000 facility

Land purchase: £245,000 released — cumulative £245,000

Foundations (15% of build): £75,000 released — cumulative £320,000

Ground floor (25% of build): £125,000 released — cumulative £445,000

First floor / roof (30% of build): £150,000 released — cumulative £595,000

Second fix (20% of build): £100,000 released — cumulative £695,000

Completion (10% of build): £50,000 released — cumulative £745,000

Retained contingency: £105,000 — cumulative £850,000

Each drawdown requires inspection and certification by an independent monitoring surveyor before funds are released, ensuring work quality and cost control. Drawdowns are flexible and aligned to the contractor’s programme and project cashflow.

Arrangement fees

Typical range: 1% to 2% of total facility.

Charged upfront (sometimes added to the loan), this covers lender processing, underwriting and legal costs. On an £850,000 loan, expect £8,500 to £17,000.

Interest rates

Typical range (2026): 7% to 12% per annum.

Rates vary based on borrower experience, project complexity, loan-to-value ratio, market conditions and lender type.

Interest calculation methods

Rolled-up interest (most common): Interest compounds monthly and is repaid at exit. This preserves cash flow during construction but increases the total repayment amount.

Serviced interest: Monthly interest payments keep the loan balance fixed but require ongoing cash flow throughout the build.

Example calculation: £850,000 loan at 9% annual interest for 18 months with rolled-up interest = approximately £120,000 total interest cost.

Other costs

Monitoring surveyor fees: £1,500 to £3,500 depending on project size and number of inspections

Valuation costs: £1,000 to £10,000 depending on project scale (case by case)

Exit fees: 1% to 1.5% of facility

Legal costs: Budget for lender’s legal costs (reviewing security, land registration, charge documentation)

Total cost example: four-unit residential scheme

Arrangement fee (1.5%): £12,750

Interest (18 months rolled): £120,000

Monitoring surveyor: £2,500

Valuation: £2,000

Legal fees: £3,000

Total finance costs: £140,250

This represents approximately 10% of GDV — a critical metric for project viability.

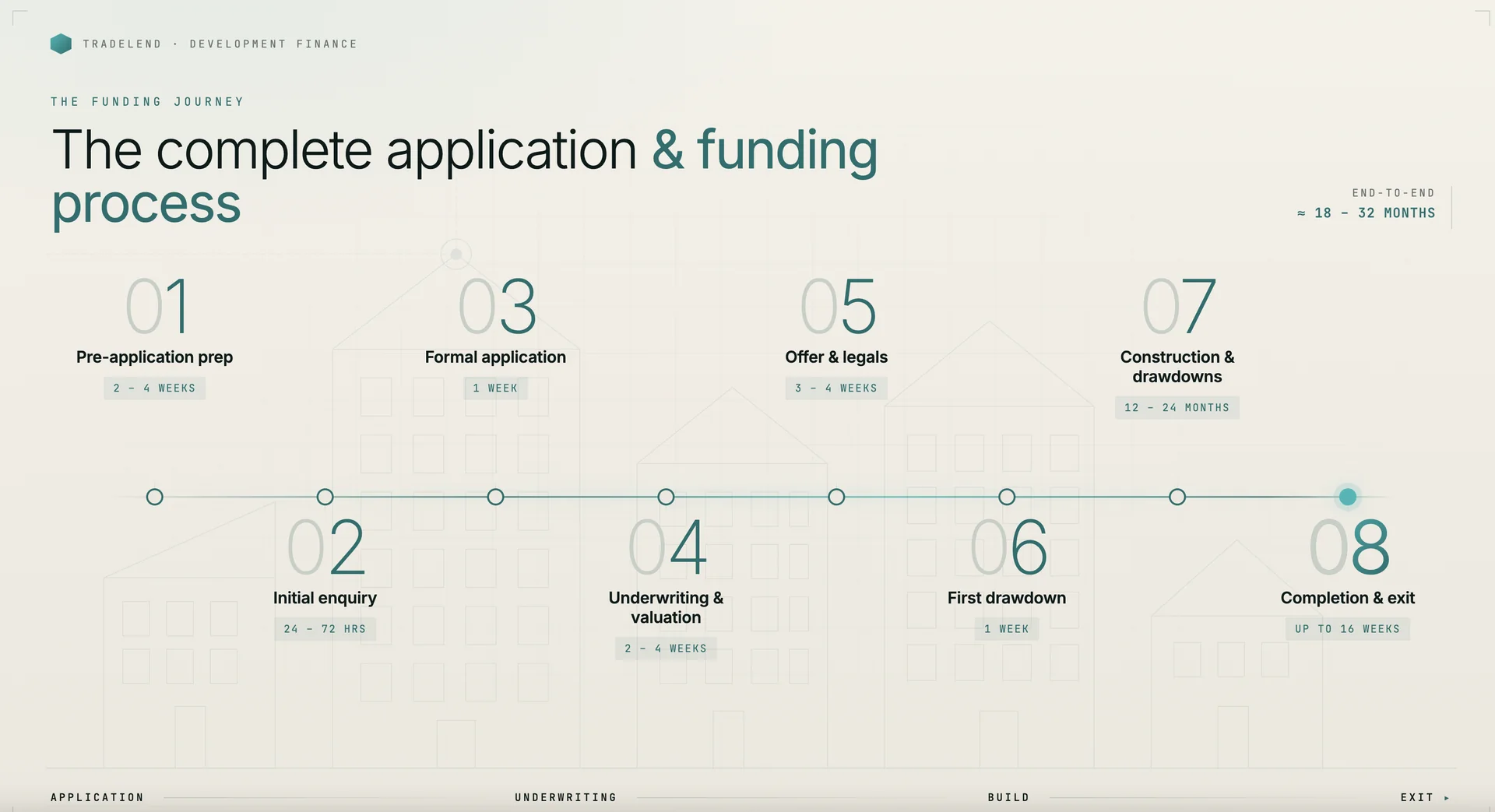

Stage 1: Pre-application preparation (2 to 4 weeks)

Before approaching lenders, gather planning documentation, project costings, development team credentials and financial information.

Stage 2: Initial enquiry and indicative terms (24 to 72 hours)

Submit outline project details to lenders or brokers. Most provide initial feedback within 1 to 3 days.

Stage 3: Formal application submission (1 week)

Complete application packs including full planning permission, detailed cost breakdown, GDV evidence, proof of deposit source and contractor details.

Stage 4: Underwriting and valuation (2 to 4 weeks)

The lender instructs an independent RICS valuation, reviews build cost viability, conducts credit checks and assesses planning risk.

Stage 5: Offer and legal process (3 to 4 weeks)

Formal offer issued, legal documentation prepared, solicitors exchange contracts on land purchase.

Stage 6: Completion and first drawdown (1 week)

Land purchase completes, first charge registered, initial advance released. Monitoring surveyor appointed.

Stage 7: Construction and staged drawdowns (12 to 24 months)

Ongoing cycle of drawdown requests, surveyor inspections, certification and fund release.

Stage 8: Practical completion and exit (up to 16 weeks)

Final inspection, warranty issued, sales complete or refinance approved, development loan repaid.

Total timeline from application to funding: typically 6 to 10 weeks. Total project timeline including construction: usually 18 to 30 months.

Residential development finance

Best for houses, apartments, flats and townhouses built for sale or rental. Higher LTV ratios are available (up to 70% GDV in some cases). Exit is usually via individual unit sales or portfolio refinance.

Commercial development finance

Best for offices, retail units, industrial buildings and mixed-use schemes. Typically lower LTV (60% GDV maximum) with higher deposit requirements (often 30% to 40% of costs).

Senior debt vs. mezzanine finance

Senior debt (first charge): Lower interest rates (7% to 10%), up to 65% to 70% LTV, first charge on security

Mezzanine finance (second charge): Higher interest rates (12% to 20%), additional 10% to 20% LTV on top of senior debt, bridges the funding gap for lower-deposit projects

Development finance vs. bridging loans

Purpose: Development finance funds ground-up construction; bridging funds property purchase or refurbishment

Term: Development 12 to 24 months vs. bridging 1 to 18 months

Funding release: Staged drawdowns vs. lump sum upfront

Build cost coverage: 100% of construction vs. not applicable

LTV: Up to 65% to 70% GDV vs. up to 75% of property value

Monitoring: Mandatory surveyor inspections vs. case by case

Best for: New builds from scratch vs. quick purchases or heavy refurb

Development finance vs. refurbishment finance

Purpose: Development funds ground-up new builds; refurbishment improves existing buildings

Structure: Development supports land plus full construction; refurbishment funds renovation only

Term: Development 12 to 24 months vs. refurbishment 6 to 18 months

Complexity: Higher (new structure) vs. lower (existing building)

Monitoring: Comprehensive surveyor oversight vs. standard inspection

Experience requirements

Lenders typically expect at least one completed development project of similar scale, extensive construction or contracting experience with residential delivery, or partnering with an experienced developer who provides a joint guarantee.

First-time developers: some specialist lenders offer products with lower LTV (55% to 60% GDV), higher deposits (35% to 40%) and a requirement for an experienced contractor with strong references.

Financial requirements

Deposit: minimum 30% to 35% of land cost, or 15% to 20% of total development costs

Credit history: satisfactory personal and business credit required

Proof of funds: bank statements, sale completions or investor commitment letters

Project requirements

Full planning permission strongly preferred

Project must demonstrate minimum 20% profit margin after all costs

Professional team: ARB-registered architect, insured contractor, chartered engineer

NHBC, Premier Guarantee, LABC or equivalent new-build warranty essential

Planning delays and condition discharge

Discharge conditions before land purchase where possible. Build time contingency into the project programme (add 2 to 4 months buffer) and budget additional finance costs for potential extensions.

Build cost overruns

Include 10% to 15% contingency in the cost plan. Obtain a fixed-price contract with the main contractor where possible. Conduct thorough site surveys and protect against inflation with material price locks.

Contractor failure or quality issues

Comprehensive contractor due diligence (references, financial checks, site visits). Ensure adequate insurance and include retention clauses in contractor agreements (typically 5% held back).

Market changes during construction

Build a GDV buffer into viability using conservative comparables. Target strong, proven markets. Pre-sell units where possible to lock in prices.

Project timeline extensions

Set a realistic construction programme from an experienced contractor. Build a 3 to 6 month time buffer into the loan term. Understand the lender’s extension policy and costs upfront.

Project overview

Site: 0.25-acre plot with full planning permission for four 3-bedroom semi-detached houses in an established residential area with strong local demand (average house price £350,000). Developer has three similar completed schemes.

Project costs breakdown

Land purchase: £350,000

Build costs (£100,000 per unit × 4): £400,000

Professional fees (architect, engineer, planning): £25,000

Statutory fees (Building Control, CIL, utilities): £18,000

Contingency (10%): £40,000

Finance costs (rolled interest and fees): £140,000

Marketing and sales: £12,000

Legal costs (purchase, sales, lender): £8,000

Warranty provider (NHBC): £6,000

Insurance (site, contractor, professional): £4,000

Utilities and site setup: £7,000

Total development costs: £1,010,000

Loan structure calculation

65% of £1,400,000 GDV: £910,000

85% of £1,010,000 costs: £858,500

Maximum loan: £858,500 (lower of the two)

Required deposit: £151,500 (15% of total costs)

Drawdown schedule

Month 0 — Land purchase: £227,500 released (cumulative £227,500)

Month 2 — Foundations: £60,000 (cumulative £287,500)

Month 5 — Ground floor and first fix: £100,000 (cumulative £387,500)

Month 8 — First floor and roof structure: £120,000 (cumulative £507,500)

Month 11 — Roof completion, weatherproof, windows: £100,000 (cumulative £607,500)

Month 14 — Second fix, internal finishes: £90,000 (cumulative £697,500)

Month 16 — Practical completion: £50,000 (cumulative £747,500)

Contingency (as needed): £111,000 (cumulative £858,500)

Finance costs detail

Facility amount: £858,500

Interest rate: 9.0% per annum

Term: 18 months

Rolled interest (£858,500 × 9% × 1.5 years): £115,898

Arrangement fee (1.5% of facility): £12,878

Monitoring surveyor (6 visits @ £400): £2,400

Valuation (RICS Red Book): £2,000

Lender legal: £2,500

Exit fee: £0

Total finance costs: £135,676

Exit and profit calculation

Gross sales proceeds (4 × £350,000): £1,400,000

Less sales costs (agent fees, legal): –£24,000

Less loan repayment (capital plus rolled interest): –£974,398

Less initial deposit: –£151,500

Net profit: £250,102

Profit margin (% of GDV): 17.9%

Return on capital invested (£151,500): 165%

Total project duration: 20 months from land purchase to final exit. This example demonstrates realistic returns accounting for all costs, professional oversight and market-standard finance terms.

Next steps: discussing your development finance needs

Key considerations before applying

Project viability must be robust: minimum 20% profit margin, realistic GDV supported by comparables, accurate build costs verified by a quantity surveyor, and proven demand through sales evidence

Team credentials are critical: lenders assess your track record, contractor strength (financial stability, experience, insurance) and the professional team’s qualifications

Planning security reduces risk: full planning permission with manageable conditions provides higher LTV, lower rates, faster approval and greater lender confidence

Exit strategy must be credible: clear evidence of exit viability through comparable sales, agent appraisals, pre-sale agreements, rental yields or tenant demand

Cash flow and contingency are essential: beyond deposit, maintain reserves for cost overruns, timing buffers for delays and personal liquidity for unexpected costs

Ready to move forward?

Property development finance provides the structured funding, professional oversight and flexible exit options that make ground-up construction viable for experienced developers and builders. Speak to experienced lenders who understand short-term construction finance to discuss your project. Get in touch with Tradelend to talk through your scheme.

Frequently asked questions

How long does it take to get development finance approved?

From initial application to funding release typically takes 6 to 10 weeks. Complex projects can extend timelines to 12 to 16 weeks.

Can I get development finance without previous experience?

Yes, but with restrictions. First-time developers typically face lower LTV (55% to 60% GDV), higher deposits (35% to 40%), and a requirement for an experienced contractor with strong references.

What happens if my project runs over budget or timeline?

Contingency funds (10% to 15% of build costs) provide the initial buffer. If exhausted, borrowers must inject additional equity. Most lenders offer 3 to 6 month extensions with additional interest (0.5% to 1% extension fee).

Do I need full planning permission before applying?

Strongly recommended. Full planning maximises LTV (up to 65% to 70% GDV), reduces interest rates and speeds approval. Outline permission or pending applications reduce LTV to 50% to 60% with a 2% to 3% rate premium.

How is interest charged?

Most commonly rolled up: interest compounds monthly and is repaid at exit, preserving cash flow during the build. Alternatively, serviced interest is paid monthly from your own funds, keeping the loan balance fixed.

What deposit do I need?

Standard requirement: 30% to 35% of land purchase price, which typically represents approximately 15% to 20% of total development costs.

Can I use development finance for commercial projects?

Yes. Key differences: lower LTV (typically 60% GDV maximum), higher deposits (30% to 40%), and a requirement for tenant demand evidence or pre-lets.

How do I exit a development finance loan?

Primary routes: sale of completed units, refinance to a long-term mortgage (buy-to-let or commercial), or onward sale to an investor.

What insurance and warranties are required?

A new-build warranty (NHBC, Premier Guarantee or equivalent), contractor PI and public liability insurance, and site and contract works insurance are all mandatory.